Update, June 29, 2021: Missouri Gov. Mike Parson on Tuesday signed into law a measure to add consumer protections and oversight to programs that make high-interest “clean energy” loans in the state. Both Missouri legislative houses voted overwhelmingly last month to support the bill.

Officials in Missouri have begun to examine and are considering measures to rein in programs that make high-interest “clean energy” loans to homeowners in the state, after a ProPublica investigation found the programs disproportionately burden borrowers in predominantly Black neighborhoods.

The Missouri Senate on Tuesday voted 31-1 on a bill to require that residential Property Assessed Clean Energy programs be reviewed by the state Division of Finance at least every other year. Currently, PACE programs have to submit annual reports to the state, but ProPublica’s investigation found little oversight.

The Senate measure would also require PACE programs to provide residential borrowers with complete information about the potential impact of their loan, including a notice that their home could be sold in a tax sale if they fail to pay the loan. The proposal now returns to the House, which has already approved a version of the bill. The legislature is scheduled to adjourn May 28. The House sponsor, Bruce DeGroot, R-Chesterfield, said the ProPublica story “opened a lot of eyes to what we’ve been saying all along: This is a consumer protection bill.”

Leaders in the city of St. Louis and in St. Louis County, meanwhile, were evaluating residential PACE lending in their communities, with the city in deliberations about whether to extend a contract with the lender that has run its PACE program and the county planning a public hearing to consider consumer protections in light of problems identified by ProPublica.

PACE programs provide financing for heating and cooling systems, solar panels and other energy efficient home improvements, and require borrowers to repay their loans in their property taxes. ProPublica found that lenders in Missouri charge high interest rates and enforce the debts through liens, leaving many borrowers at risk of losing their homes at forced public tax sales. The loans carry a median annual percentage rate of 10% and can stretch to 20 years, burdening some borrowers with interest and fees that sometimes exceed the cost of the project — and sometimes the value of their home.

Supporters of PACE say the program makes loans in predominantly Black neighborhoods in Missouri where banks typically do not do much business. Lenders say their rates tend to be lower than some credit cards and payday lenders, other avenues of credit for low-income borrowers.

ProPublica’s analysis found that more than 100 homes with PACE loans in metropolitan Kansas City and St. Louis were at risk of being sold at public auctions after their owners fell at least two years behind on payments. Of those, at least 29 were slated for auction this year.

ProPublica found that 28% of borrowers in predominantly Black neighborhoods were at least one year behind in repaying their PACE loans, compared with 4% in mostly white areas. Borrowers in predominantly Black neighborhoods also paid a larger share of their home value toward interest and fees, sometimes more than county appraisers said their homes were worth.

Officials with Ygrene Energy Fund, the most prominent lender in the St. Louis market, and Missouri Clean Energy District, or MCED, which operates mostly in the Kansas City area and in St. Charles County outside St. Louis, challenged ProPublica’s use of local government appraisals to compare with the size of a loan. Many lenders instead rely on private appraisers, whose valuations often are higher.

The Senate proposal would require PACE programs to base loans on appraisals from local governments, sharply curtailing the availability of PACE to the owners of homes with very low property values. That would prevent some of the lopsided loan-to-value ratios ProPublica highlighted.

David Pickerill, executive director of MCED, said the change “reduces the eligibility of many properties, especially in minority areas of metropolitan cities.” But he said MCED felt that the Senate proposal overall was “clear ratification of the importance” of the 2010 law that created PACE.

Ygrene declined to comment on the legislation or on the actions of local leaders in St. Louis and St. Louis County. But a company spokesman defended the loan program. “What’s lost in your reporting is that PACE provides important (or real) property improvements when a homeowner needs it the most, like furnaces in cold snaps, air conditioning during sweltering summers, and roof replacements during the rain,” the spokesman, Rob O’Donnell, said in an email.

State oversight would mark a significant change for Missouri’s residential PACE program. ProPublica found that weak oversight by local boards of directors has allowed lenders and contractors to sometimes act in ways that are not in the best interest of borrowers, with few repercussions. Some borrowers said they signed up for PACE loans they couldn’t afford out of desperation. Others said they didn’t understand what they were signing or didn’t grasp how the loans would affect their property taxes. Board members for the programs that serve the St. Louis and Kansas City areas said they allowed lenders to run the operations.

After ProPublica’s story, St. Louis County Executive Sam Page removed Jim Holtzman, chair of the county’s PACE board and a Page critic. Holtzman, who had continued to serve on the PACE board though his term had expired in 2019, told ProPublica he did not ask many questions of Ygrene. He had said it wasn’t his “responsibility to go hunt down” information about delinquent loans.

“I served on the clean energy development board for six years as chairman. I’m glad that somebody else will be taking over at this point,” Holtzman said Thursday.

PACE debt has affected the communities in St. Louis County’s 1st Council District surrounding Ferguson, where about 40% of Ygrene borrowers were at least a year late on their property taxes.

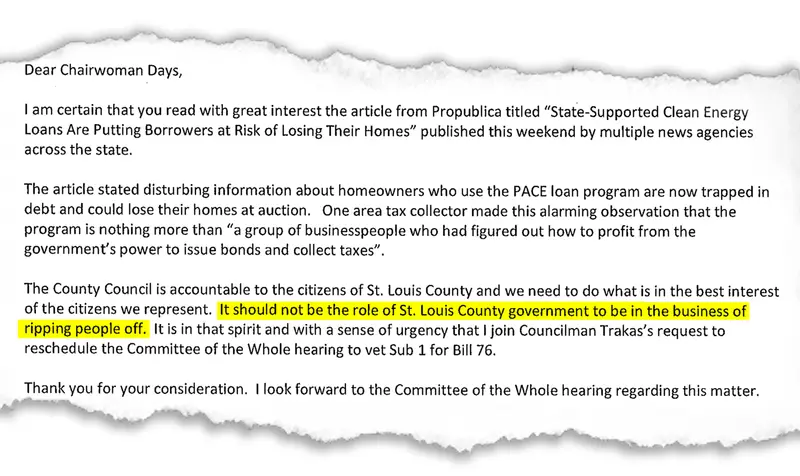

The St. Louis County Council scheduled a May 18 hearing to investigate its PACE program after Councilwoman Kelli Dunaway said in a letter to the council chair, Rita Heard Days, that ProPublica’s findings were “disturbing” and the county government should not be in “the business of ripping people off.”

The city of St. Louis — where one of every three borrowers with a PACE loan is late paying their property taxes — has opened Ygrene’s contract to bid. A committee, which includes representatives from the mayor’s office, city comptroller and the board of aldermen, as well as the PACE program, met Tuesday to evaluate proposals from Ygrene and other bidders. The committee did not name the other bidders and excluded the public after a general discussion of the program. The committee said later it did not take any action following the closed discussion.

On the other side of the state, Jackson County Executive Frank White Jr. vetoed a bill that would have allowed a second PACE program to operate in much of the Kansas City area, saying he was troubled that ProPublica found “significant differences between how the program is impacting majority white and majority Black areas” of the county. Despite voting 9-0 to approve the bill, the legislature declined to override White’s veto. Legislators said they needed to review the matter.